Japan cuts interest rates and reduces debt + oil price at $85, can your US stock holdings withstand it?

- June 19, 2025

- Posted by: Macro Global Markets

- Category: News

1. The Bank of Japan maintains an easing tone and gradually promotes the plan to reduce government bond purchases

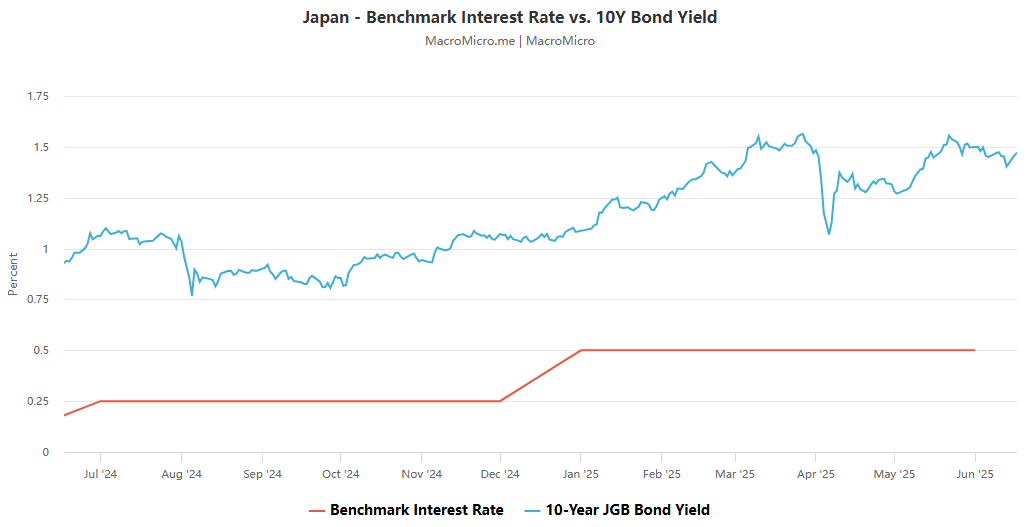

On June 17, the Bank of Japan announced that it would maintain its target interest rate at 0.5%, keeping its monetary policy unchanged for the third consecutive time, in line with market expectations. The bank voted 8 to 1 to extend the existing bond reduction plan until March 2026, and reduce the monthly purchase of government bonds by about 200 billion yen per quarter from April 2026 until the monthly purchase scale is reduced to about 2 trillion yen from January to March 2027.

The policy statement pointed out that the Japanese economy as a whole is showing a moderate recovery trend, with exports and industrial production remaining flat, equipment investment growing moderately due to improved corporate profits, and private consumption remaining resilient amid an improved employment environment, but residential investment is weak. In terms of prices, the core CPI rose by about 3.5% year-on-year, mainly affected by the transmission of wage increases and food prices (such as rice), but as import prices and food price increases weaken, core inflation is expected to be sluggish in the short term and gradually approach the price stability target in the medium and long term as the economy recovers. The Bank of Japan emphasized that it will reduce government bond purchases in a predictable manner while retaining flexibility to maintain market stability. If long-term interest rates rise rapidly, it will respond by increasing purchases or fixed interest rate operations.

2. Expectations of the Fed remaining on hold rise, and concerns about policy lags loom

The market generally expects the Fed to keep interest rates unchanged at its meeting early Thursday morning, and the implied probability of CME interest rate futures has soared to 99.3%. However, the core PCE price index is still hovering at a high level of 3.2% year-on-year, which is still significantly away from the Fed’s 2% inflation target. Atlanta Fed President Bostic recently publicly stated that it is necessary to see core inflation below 2.5% for at least three consecutive quarters before considering adjusting monetary policy. It is worth noting that the current geopolitical risks continue to ferment: the United States’ new round of tariff lists on China’s semiconductor industry chain is about to land, and the Iran-Israel conflict has caused Brent crude oil futures prices to hit a nearly 18-month high. This has put the Fed in a dilemma between “fighting inflation” and “preventing recession.” US President Trump even sent three tweets on social media, accusing Powell of “sticking to high interest rates is economic suicide.” This political intervention has further exacerbated policy uncertainty.

Signs of weakness in the labor market are forming a vicious cycle: the number of first-time unemployment claims last week climbed to 238,000, the highest since November 2023; the ADP employment report showed that the private sector added only 145,000 jobs, far below the market expectation of 200,000. In terms of wage growth, the year-on-year increase in average hourly wages has slipped from 4.2% at the beginning of the year to 3.7%, and the purchasing power of real wages has continued to decline. According to the latest forecast model of the New York Federal Reserve, the probability of the unemployment rate exceeding 4.6% by the end of 2026 has reached 68%, which is a significant increase from the Fed’s forecast of 4.3% in March. The real estate market is also under pressure, with the house price index falling for seven consecutive months, and the net worth of American households has shrunk by $1.2 trillion. Consumer behavior has changed accordingly, with the savings rate jumping from 4.1% in the same period last year to 5.8%, and credit card consumption falling by 1.3% month-on-month. This precautionary savings behavior is weakening the role of the consumption engine in driving the economy.

Signs of weakness in the labor market are forming a vicious cycle: the number of first-time unemployment claims last week climbed to 238,000, the highest since November 2023; the ADP employment report showed that the private sector added only 145,000 jobs, far below the market expectation of 200,000. In terms of wage growth, the year-on-year increase in average hourly wages has slipped from 4.2% at the beginning of the year to 3.7%, and the purchasing power of real wages has continued to decline. According to the latest forecast model of the New York Federal Reserve, the probability of the unemployment rate exceeding 4.6% by the end of 2026 has reached 68%, which is a significant increase from the Fed’s forecast of 4.3% in March. The real estate market is also under pressure, with the house price index falling for seven consecutive months, and the net worth of American households has shrunk by $1.2 trillion. Consumer behavior has changed accordingly, with the savings rate jumping from 4.1% in the same period last year to 5.8%, and credit card consumption falling by 1.3% month-on-month. This precautionary savings behavior is weakening the role of the consumption engine in driving the economy.

From the perspective of monetary policy game, if the temporary inflation disturbance caused by trade frictions and geopolitical conflicts is excluded, core service inflation has been below 2.2% for five consecutive months, which meets the conditions for interest rate cuts. The market generally expects the Federal Reserve to release a policy shift signal at the Jackson Hole Global Central Bank Annual Meeting in August, but economists at the Bank of Montreal warn that if the waiting time is too long, the reality that the manufacturing PMI has been below the boom-bust line for 14 consecutive months may accelerate the economic recession. In sharp contrast, the stress test released by State Street Global Advisors shows that the current vulnerability index of the US economy has reached the second highest level since the 2008 financial crisis, and it is recommended that the Federal Reserve start a 25 basis point interest rate cut cycle at the June interest rate meeting to avoid the risk of a “hard landing” of the economy.

3. As the conflict between Iran and Israel escalates, US stocks face a triple risk test

Royal Bank of Canada (RBC) pointed out that the Iran-Israel conflict could drag down U.S. stocks through three major channels:

- Valuation risk : When geopolitical uncertainty rises, the S&P 500 P/E ratio tends to shrink. The current stock price is close to a record high, and the valuation did not fall to the “cheap” range during the tariff crisis in April, and is highly sensitive to negative news.

- Market sentiment is frustrated : The escalation of tensions in the Middle East could reverse the recent improvement in investor sentiment. Businesses and consumers have become cautious – CEO confidence fell to a three-year low in the second quarter, consumers are still concerned about tariffs and extreme weather, and the frequency of mentioning geopolitics in earnings conference calls has increased.

- Surging oil prices push up inflation : If the conflict leads to supply disruptions in the Middle East, oil prices may rise further. RBC expects core PCE inflation to rise to 4%, suppressing the Fed’s room for rate cuts in 2025 (possibly only twice), which in turn will hit stock market valuations that rely on expectations of rate cuts.

The bank’s stress test shows that the fair value of the S&P 500 index may fall to 4,800-5,200 points at the end of the year, which may be a 20% drop from the current level, and its previously raised year-end target price of 5,730 points also has a 4% downside. Although most Wall Street institutions are still optimistic about the stock market’s positive growth in 2025, JPMorgan Chase, Citigroup and others have lowered their expectations to the 6,000-6,300 point range.

Conclusion

At present, the global financial market is deeply trapped in a complex dilemma of monetary policy divergence and geopolitical risks: the Bank of Japan has gradually reduced its YCC yield curve control policy against the backdrop of a mild recovery in domestic consumption and core inflation above 2% for 19 consecutive months, and the 10-year Treasury yield has exceeded the key threshold of 0.8%, triggering a chain reaction in the global bond market; the Federal Reserve, faced with contradictory signals of a 3.7% year-on-year increase in the core PCE price index and unexpected non-farm payroll data, has fallen into a dilemma between “the urgency of anti-inflation” and “the demand for a soft landing of the economy”, and the market’s expectation of the probability of suspending interest rate hikes in June has risen to 89%; at the same time, the Iran-Israel conflict continues to escalate, the Iranian Revolutionary Guard intervenes in the Gaza Strip, and the Red Sea shipping disruption has caused the Brent crude oil futures price to exceed US$85 per barrel, which has suppressed the valuation of the S&P 500 index with a price-to-earnings ratio of up to 25 times. The resonance effect of the monetary policy shift and geopolitical conflicts is forcing investors to recalibrate their risk models and seek a new balance in asset allocation under the dual impact of interest rate fluctuations and risk aversion.